Apr 2026 · AI Strategy

The numbers are big. The policy change is bigger. And if you're building anything with AI in India right now, you need to understand both.

Built by an AI engineer. Not a journalist.

NotebookLM Podcast

India's Billion-Dollar Sovereign Compute Surge

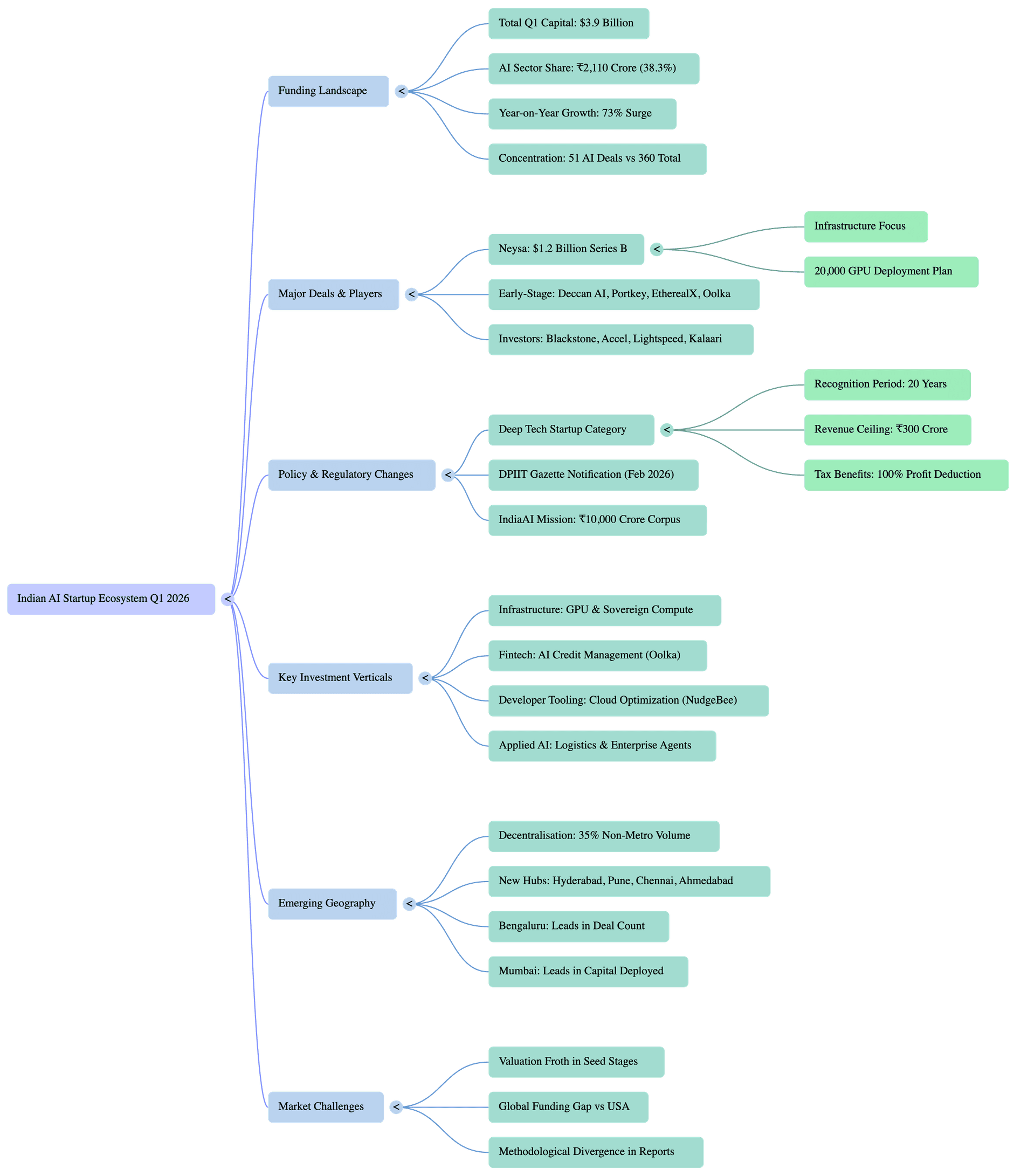

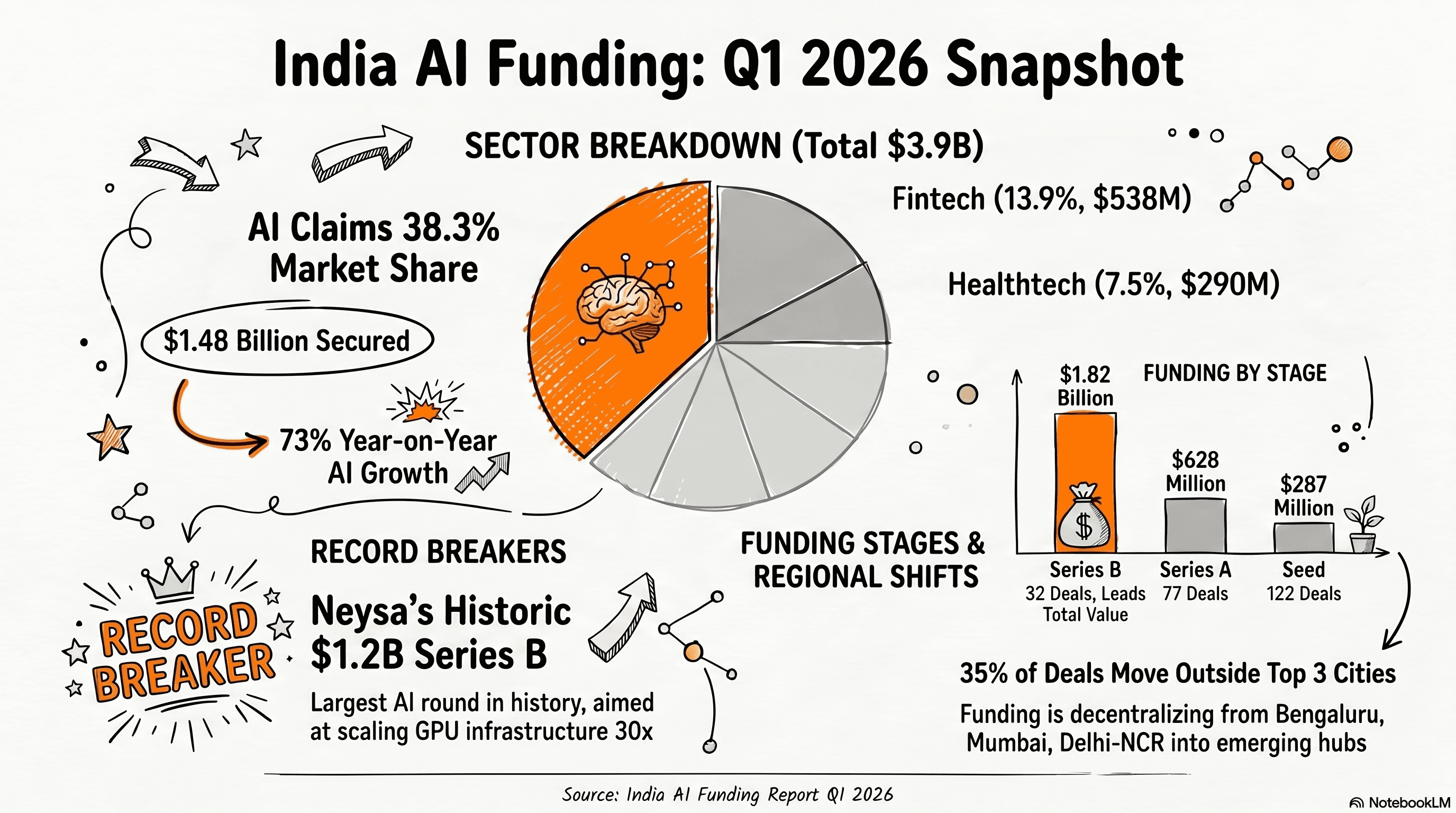

Indian AI startups raised ₹2,110 crore in Q1 2026. That's a 73% year-on-year surge, and it made artificial intelligence the single largest magnet for venture capital in the country this quarter. Not fintech, not e-commerce, but AI.

I've watched a few of these “India AI moment” cycles come and go. This one feels different.

What ₹2,110 crore sits inside

The full picture of Q1 2026 Indian startup funding is roughly $3.9 billion across about 360 deals, one of the strongest quarters since 2022. AI captured $1.48 billion of that, accounting for 38.3% of all capital deployed across just 51 deals. Fintech came in second at $538 million. Healthtech third at $290 million.

Fewer deals, more money. That's not noise. That's a deliberate signal from investors about where they want to concentrate.

One deal alone swung the numbers dramatically: Neysa's $1.2 billion Series B, led by Blackstone alongside Teachers' Venture Growth, TVS Capital, 360 ONE Asset, and Nexus Venture Partners. It's the largest AI funding round in Indian startup history. It came with a plan to deploy over 20,000 GPUs inside India, a country that currently has fewer than 60,000 GPUs total. Blackstone estimates that number needs to grow 30x in the coming years. Neysa is positioning itself as the infrastructure layer for that buildout.

Strip out Neysa and the AI funding picture still holds. Early-stage deals like Deccan AI, Portkey, EtherealX, and Oolka all closed rounds in the same quarter. The concentration isn't just one anomalous mega-round. The tide is coming in from multiple directions.

The policy change nobody talked about enough

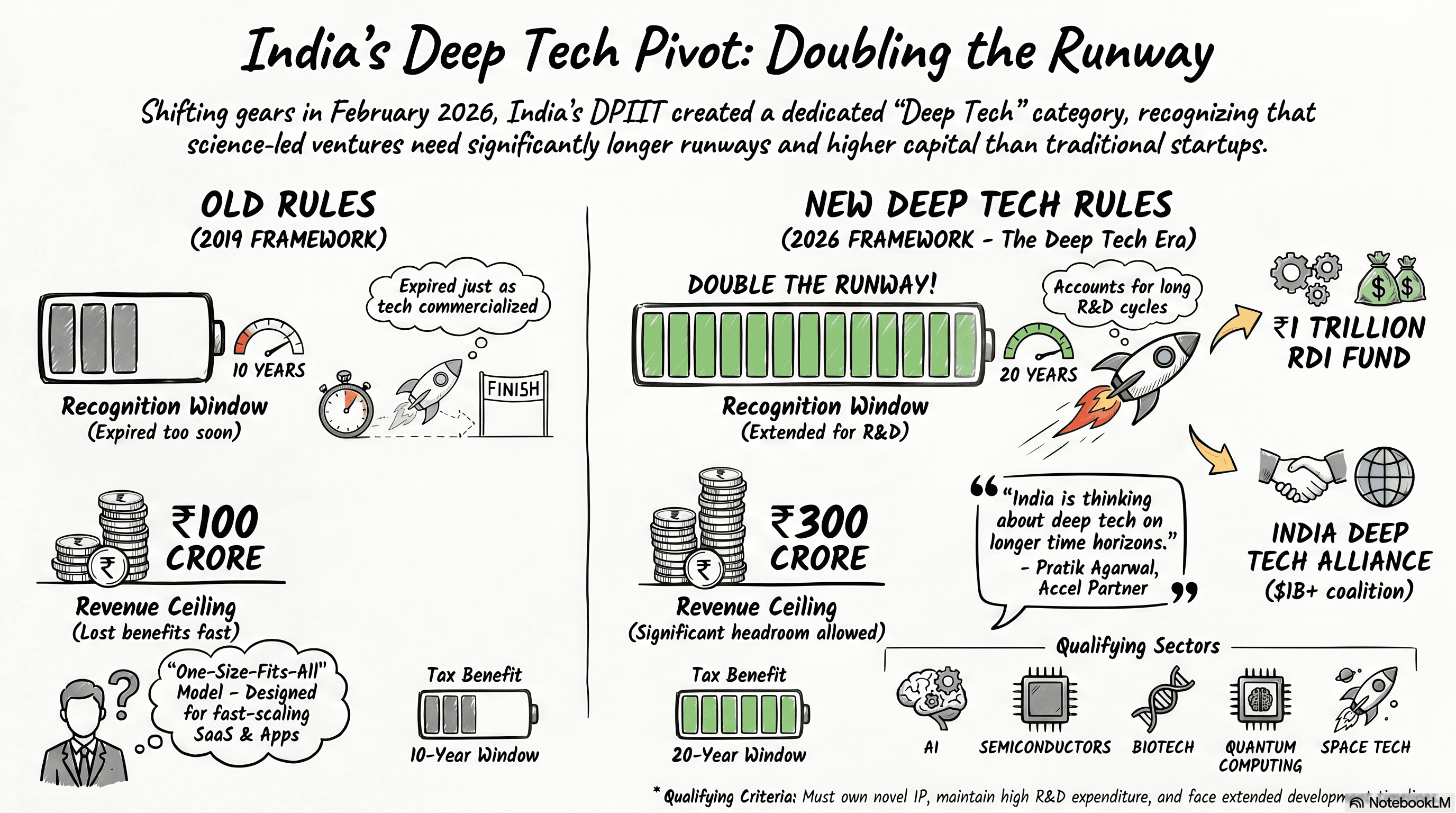

Two weeks before the Neysa round closed, the Government of India quietly rewrote the rules for who counts as a startup.

On February 4, 2026, DPIIT issued a gazette notification that replaced the 2019 startup framework. For general startups, the revenue threshold for maintaining startup status doubled, from ₹100 crore to ₹200 crore, with the recognition period staying at 10 years.

But for a new, formally recognized category called Deep Tech Startups, the rules are different. AI, semiconductors, biotech, quantum computing, space tech. Companies working in these fields now get 20 years of startup recognition (up from 10), a revenue ceiling of ₹300 crore (up from ₹100 crore), and access to Section 80-IAC tax benefits across that entire extended window: a 100% profit deduction for three consecutive years, valid within a 20-year horizon.

Think of it like a battery. Previous policy gave deep tech founders a 10-year charge before their startup benefits expired. The new framework doubles that charge and triples the voltage capacity.

This matters more than it looks. Deep tech companies don't build on software timelines. A semiconductor company or a biotech firm might spend 7 years just reaching clinical or commercial validation. An AI infrastructure company like Neysa, founded in 2023, still sub-₹25 crore in revenue, now valued at $1.4 billion, doesn't fit neatly into a 10-year recognition window either. The old framework was designed for SaaS startups and consumer apps. The new one acknowledges that science-led companies operate differently. I've talked to founders who quietly gave up equity to non-Indian structures specifically to escape this cliff. That workaround just became unnecessary.

Who's actually getting the money

Strip away the Neysa headline and the Q1 2026 deal flow tells a more nuanced story about what Indian investors are actually backing.

Infrastructure and compute: Neysa's round is a bet on the picks-and-shovels layer, GPU capacity, sovereign compute, enterprise AI workloads that need India-resident data. Blackstone's thesis mirrors what they did globally with QTS Realty and AirTrunk: own the substrate.

Credit and financial services AI: Oolka raised ₹130 crore from Accel and Lightspeed for AI-powered credit management targeted at MSMEs and new-to-credit borrowers. Credit underwriting is one of the highest-value near-term applications for AI in India. The data asymmetry in lending is massive, and AI closes that gap profitably.

Cloud operations and developer tooling: NudgeBee raised $3 million from Kalaari Capital for AI-powered cloud cost optimization. Portkey attracted early-stage interest for its AI gateway infrastructure. These aren't consumer plays. They're B2B tools that slot directly into engineering workflows.

Agentic and applied AI: The broader deal flow, including Deccan AI, EtherealX, and The Guild, reflects early bets on vertical AI agents across logistics, enterprise automation, and domain-specific workflows.

The common thread: investors aren't funding general AI. They're funding AI with a specific, near-term customer and a clear revenue path. The math changes completely when you can point to a paying enterprise on day one.

The forces underneath

A few forces are compounding each other here in a way that makes Q1 2026 feel like an inflection, not a blip.

The India AI Impact Summit in February 2026 triggered over $200 billion in investment commitments across Adani, Microsoft, and government-backed funds. The IndiaAI Mission's ₹10,000 crore corpus is the most direct catalyst. Public capital de-risks private bets: when the government is a committed buyer of AI compute and services, early-stage investors have a visible floor on demand.

The India Deep Tech Alliance, a $1 billion-plus coalition of Accel, Blume Ventures, Celesta Capital, Premji Invest, and others with NVIDIA as an adviser, represents coordinated private capital with a multi-year thesis on Indian deep tech. This isn't a fund that makes one bet and moves on. It's a structural commitment from the investors who matter most.

And India's macroeconomic fundamentals are hard to argue with. Strongest GDP trajectory among major economies. UPI processed 22.6 billion transactions in March alone. 1.4 billion people. The addressable market scale is something Southeast Asian rivals genuinely cannot match.

The geographic footprint is fracturing too. Cities outside Bengaluru, Mumbai, and Delhi-NCR now account for more than 35% of total deal volume. Hyderabad, Pune, Chennai, and Ahmedabad have graduated from satellite office locations to genuine startup formation hubs, with local angel networks and indigenous deal creation. Bengaluru still leads on deal count. But if you're building an AI company in Hyderabad today, you're not at a geographic disadvantage the way you would have been three years ago.

The honest caveat

Not every data point points the same direction.

Inc42's Q1 report, which uses a tighter definition of “tech startup” (excluding non-tech sectors), showed a 26% year-on-year decline to $2.3 billion in tech-specific funding. The divergence comes down to methodology. Entrackr's broader dataset captures cross-sector rounds including AI infrastructure, while Inc42 focuses more narrowly on software and consumer tech.

Early-stage seed valuations have crept ahead of revenue metrics, creating a potential 12-18 month correction window at that stage. AI deals are not immune to this. The froth is real.

And India's deep tech funding recovered to $1.65 billion in 2025, up from $1.1 billion in each of the two prior years. It's still roughly 1/90th of what the US deployed in deep tech in 2025 ($147 billion per Tracxn). The policy changes are real. The gap is also real. I'd rather have both facts on the table than pretend one cancels out the other.

What this means if you're building

The 20-year deep tech recognition window removes a financial cliff that killed earlier cohorts. I watched AI companies from 2015 to 2018 hit revenue growth just as their startup benefits expired, which created a tax and compliance burden that compressed margins at exactly the wrong moment. That cliff is now 20 years away for anyone who qualifies as deep tech under the new DPIIT framework.

The sectors drawing the most investment are defensible because they solve problems with measurable, recurring value. Investors funding AI infrastructure, credit underwriting, and agentic enterprise workflows aren't making speculative bets on model benchmarks. They're funding distribution into large existing markets.

If you're mapping where to focus: the compute layer (Neysa, GPU infrastructure), the application layer for BFSI (credit, collections, compliance), and vertical agents for regulated industries (healthcare, logistics, manufacturing) are where capital is concentrating. The macro is pointing you toward those bets.

The takeaway

India pulled in nearly $4 billion in startup funding in Q1 2026. AI took 38% of it. A new regulatory framework just doubled the runway for deep tech founders. The country's GPU infrastructure is about to scale 30x.

The question isn't whether India is a credible AI market anymore. Blackstone answered that in February, with a $600 million equity check. The question now is what you build on top of this infrastructure, and how fast you move before the obvious plays get crowded.